How LNG imports and terminals support UK gas supply

In 2024, 11% of the UK’s gas demand was met by imports of super-cooled natural gas, shipped thousands of miles across the Atlantic from the US.

As North Sea gas production continues to decline, the UK has become increasingly dependent on liquefied natural gas (LNG) imports from the global market, despite their higher costs and environmental impact.

This guide explains the crucial role of LNG in the UK energy market. Here’s what we cover:

- What is Liquefied Natural Gas (LNG)?

- How LNG is produced and transported

- LNG terminals and infrastructure in the UK

- Where does the UK’s gas come from?

- The impact of LNG imports

- The future of LNG in the UK

What is Liquefied Natural Gas (LNG)?

Liquefied natural gas (LNG) is natural gas converted into a liquid state by cooling it to −162 °C.

In this liquefied form, LNG occupies around 600 times less volume than regular natural gas, making it significantly more efficient to transport across oceans.

In 2024, there are more than 700 active ships with specialised cryogenic tanks designed to transport substantial volumes of LNG, called LNG carriers.

Transporting LNG by ship enables countries with a surplus of natural gas to export it to nations anywhere in the world.

How LNG is produced and transported

There are no large-scale LNG production facilities in the UK. Instead, the UK relies on importing LNG produced in the United States.

The following step-by-step process explains how LNG is produced in the US, transported across the Atlantic, and fed into Britain’s gas distribution network.

Natural gas extraction

Natural gas forms over millions of years from the decomposition of organic matter buried beneath layers of sediment.

Unlike the UK, the US has abundant natural gas formations, particularly in Texas and Appalachia.

Most natural gas in the US is extracted through the process of fracking, in which high-pressure water, sand, and chemicals are pumped into rock formations to release the gas.

The extracted gas is processed into a purified product that is around 95% methane, meeting both UK and US pipeline quality standards.

Transportation to US LNG liquefaction terminals

Natural gas extraction facilities feed processed natural gas into the US interstate transmission network.

Using this long-distance pipeline network, the extracted gas is delivered to LNG liquefaction facilities on the coastline of Texas and Louisiana.

LNG liquefaction

At a liquefaction facility, natural gas is cooled from ambient temperature down to −162 °C, at which point the methane turns into its liquid form, LNG, reducing its volume by a factor of 600.

The LNG is then transferred onto LNG carriers. Aluminium tanks on these ships hold the LNG in its liquid form throughout the journey.

Transportation by LNG carrier

LNG carriers cross the Atlantic on a journey that typically takes 9–14 days, depending on the weather and routing.

A modern large LNG carrier can transport about 170,000 cubic metres of LNG in a single voyage, enough to supply the annual gas needs of around 90,000 UK households.

The ships can unload the LNG at one of the UK’s three LNG regasification terminals.

Regassification and distribution

Regasification occurs at the receiving LNG import terminal, where specialised units reheat LNG to ambient temperature to turn it back into a gas.

The regasification facilities feed the imported natural gas into Britain’s National Transmission System pipeline infrastructure, from where it can be transported nationwide to consumers.

Domestic and business energy suppliers purchase the gas on the National Transmission System either through direct agreements with the LNG importers or via the wholesale gas market.

LNG terminals and infrastructure in the UK

The UK’s LNG infrastructure is concentrated in its three import terminals, which enable LNG to be brought in by ship and fed into the gas distribution network.

LNG import terminals overview

The UK has three main LNG terminals that handle the import, storage, and regasification of LNG, as well as its injection into the UK’s national gas transmission system:

- Isle of Grain LNG Terminal, Kent – A facility on the River Medway (a tributary of the Thames) with two jetties allowing ships to unload their LNG. The facility can regasify up to 645 GWh of natural gas each day for delivery into the NTS.

- South Hook LNG Terminal, South Wales – Located in Milford Haven, this is the largest LNG regasification facility in Europe. It has the capacity to process 20% of the UK’s daily natural gas needs.

- Dragon LNG Terminal, South Wales – This smaller regasification facility, also in Milford Haven, has the capacity to receive up to 96 LNG ships each year.

How LNG is fed into the National Transmission System (NTS)

Each of the UK’s three LNG import terminals is directly connected to the National Transmission System (NTS), a high-capacity national gas pipeline.

The NTS delivers the imported natural gas to three main user groups:

- Gas power stations – Facilities that combust natural gas to generate electricity.

- Industrial users – Such as glass production facilities and oil refineries, which require vast amounts of natural gas and are connected directly to the NTS.

- Domestic and other businesses – The NTS connects to regional Gas Distribution Networks and Independent Gas Transporters, which provide a gas supply to local homes and businesses.

Exports to the European content

Britain’s National Transmission System for gas is connected to its European neighbours via three undersea pipelines to Belgium, the Netherlands, and the Republic of Ireland.

These connections allow LNG received in the UK to be sold into the European market when there is surplus gas on the NTS. In 2024, the UK exported 118 TWh of natural gas to Europe.

Where does the UK’s gas come from?

This section explains the crucial role of LNG imports in the UK energy market in meeting the shortfall in domestic natural gas production and enhancing energy security.

Declining domestic gas production

The UK has its own source of natural gas, which it extracts from gas fields in the North Sea. In the early 2000s, gas from the North Sea met the entirety of the country’s gas demand.

However, over the last two decades, production in the North Sea has steadily declined due to the depletion of fields first discovered in the 1960s. In 2024, North Sea gas production met only around half of the UK’s gas demand.

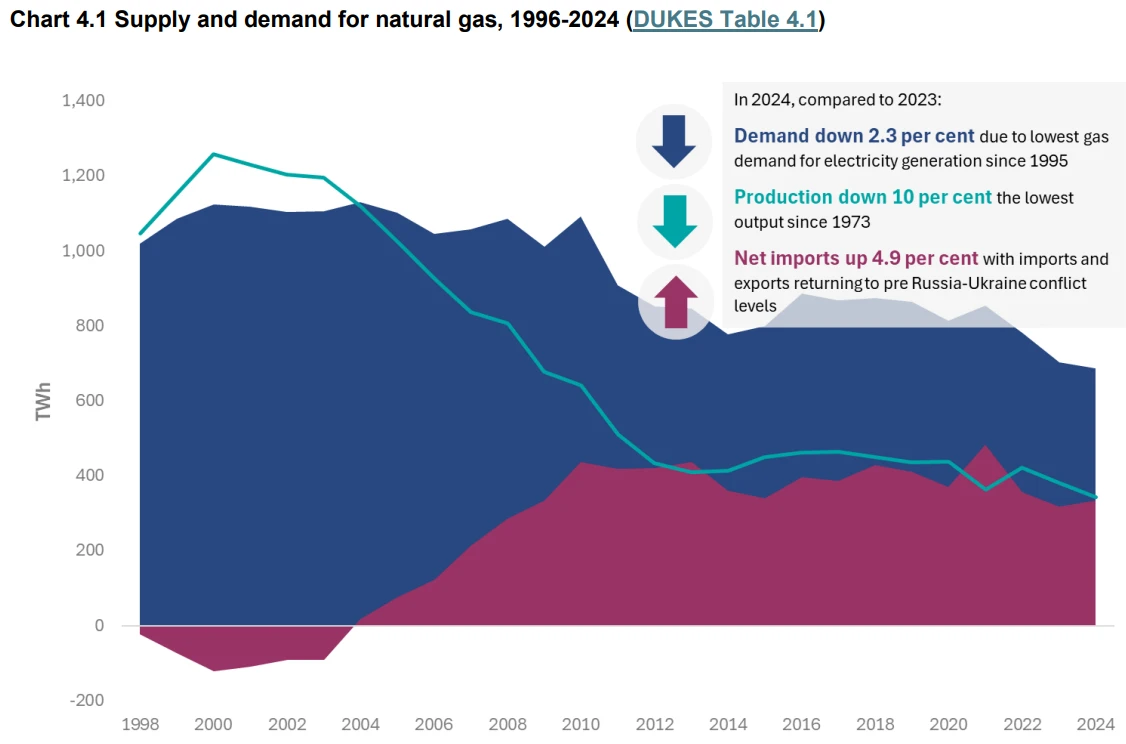

This decline has left the UK dependent on importing gas to meet its needs. The graph below shows how UK gas production and exports have changed over the past 30 years.

Source: Gov.uk – UK Gas Statistics 2024

The importance of LNG gas imports

To meet domestic gas demand, the UK imported 453 TWh of gas in 2024. The majority of these imports came via pipelines from Norwegian gas fields (75%), with the remaining 25% coming from LNG imports.

The graph below shows the sources of imported natural gas in 2024.

Source: Gov.uk – UK Gas Statistics 2024

💡The imports from Norway are transported via the import-only Langeled Pipeline, which connects the UK to Norway’s offshore gas fields.

In 2024, LNG imports fell by 47% compared with 2023, yet they remained a significant and essential source of gas for the UK.

Why LNG is crucial for energy security

LNG imports have been essential in ensuring the UK can meet its gas demand during supply shocks, such as the 2022 UK energy crisis. During the crisis, a combination of factors led to the need for increased LNG imports:

- A surge in natural gas demand post-COVID, as economies reopened and energy consumption rose.

- Disrupted gas supplies from Russia due to the ongoing conflict in Ukraine, which led to a significant reduction in gas flows to Europe.

- The closure of the Rough natural gas storage facility, which had previously provided a strategic buffer for the UK during periods of high demand.

During the crisis, LNG carriers were redirected at sea to provide an important back-up supply of gas, preventing even sharper price rises.

LNG regasification facilities enable the UK to import natural gas from a variety of countries, including the US, Qatar, Algeria, and Nigeria. This reduces dependence on a small number of pipeline suppliers (such as Norway) and lowers vulnerability to political, technical, or weather-related disruptions on fixed routes.

The impact of LNG imports

This section explores the wider economic and environmental consequences of the UK’s reliance on LNG imports.

Higher energy costs for homes and businesses

LNG is inherently more expensive than pipeline gas due to the additional processing and energy required for liquefaction, transportation, and regasification.

Since LNG makes up a significant portion of the gas available on the National Transmission System, it increases overall wholesale gas prices.

Reliance on LNG makes wholesale gas purchases more expensive for business gas suppliers, who pass this cost on to consumers in the form of higher domestic and business gas prices.

In 2024, 33% of the UK’s electricity was generated from gas power stations, so increases in wholesale natural gas prices also affect domestic and business electricity prices.

💡At Business Energy Deals, we specialise in helping businesses find the cheapest energy prices. Discover how much you could save with our free, no-obligation business electricity comparison service.

Higher carbon emissions

The additional processing and transportation steps involved in importing LNG make it significantly more carbon-intensive than pipeline gas.

Substantial methane leakage occurs during liquefaction, regasification, and transportation by sea.

Analysis from the North Sea Transition Authority, shows that the UK’s domestic gas production emits 21 kg CO₂ per barrel of oil equivalent (boe). In contrast, imported LNG emits nearly four times as much, 79 kg CO₂ per boe, by the time it reaches the UK for consumption.

While LNG imports are crucial for energy security, each time the UK relies on them to meet demand, it complicates the country’s legally binding commitment to achieve net zero, which requires the complete phase-out of unabated natural gas use.

The future of LNG in the UK

The UK government is legally committed to phasing out unabated fossil fuels, including LNG, by 2050.

However, current government policy is to use LNG as a strategic, temporary bridge fuel during the transition to alternative low carbon energy sources. The government is investing in LNG infrastructure and plans to continue using it for the coming decades. This includes:

- Continued LNG imports from strategic partners such as the US, Qatar, and others.

- Ongoing investment in LNG terminals to maintain import capacity, ensuring flexibility in gas sourcing.

- Integrating Carbon Capture and Storage (CCS) technology into LNG facilities to reduce emissions during the transition.

The UK government is pursuing three main policies to eliminate gas consumption in the medium term:

- Electricity generation transition – By 2030, the government aims to eliminate the contribution of gas power stations to electricity generation through continued development of UK wind farms and the construction of the Sizewell C and Hinkley Point C nuclear power stations.

- Carbon-neutral gas production – Promoting domestic production of carbon-neutral gas supplies through the Green Gas Support Scheme and encouraging the development of green hydrogen generation.

- Gas-free heating – Eliminating domestic and commercial gas consumption by encouraging the adoption of technologies such as heat pump systems, which use electricity to replace the gas boilers widely used for heating properties.

- Share: